-

RoleSenior Product Designer

-

ScopeEnd-to-end product design (mobile + web)

-

PlatformConsumer telecom + fintech ecosystem

Impact

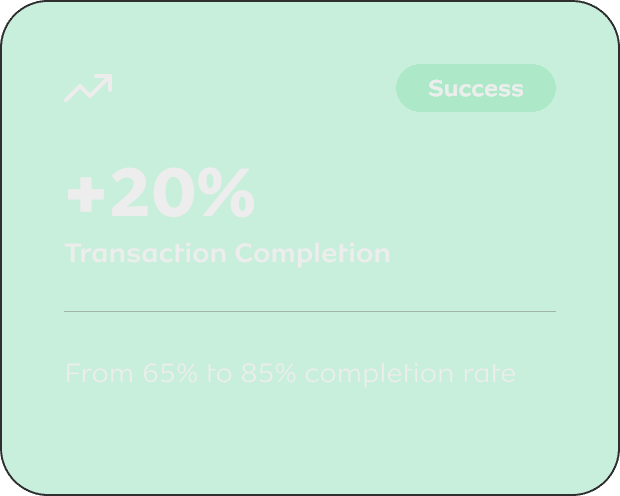

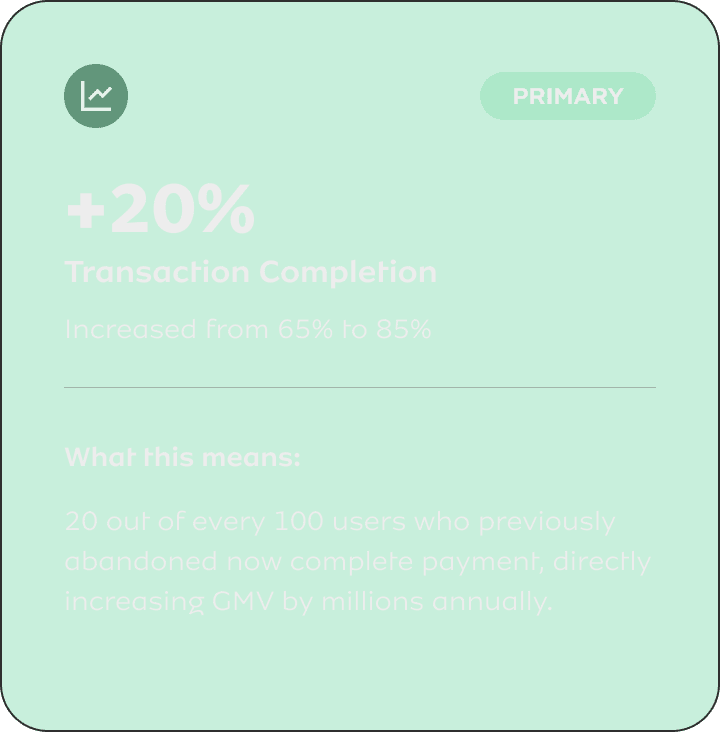

- +20% transaction completion

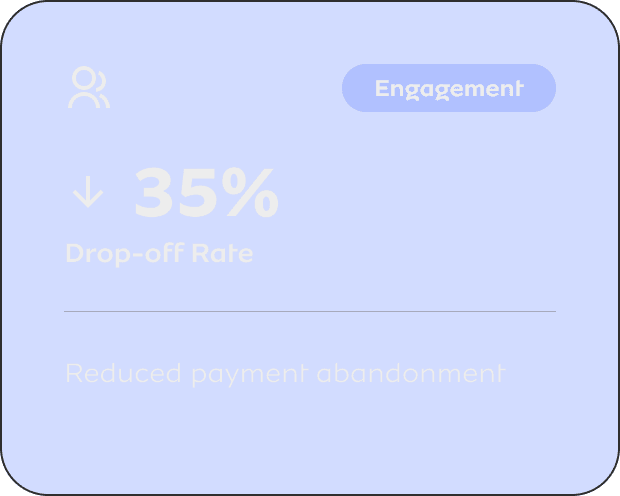

- Reduced drop-offs

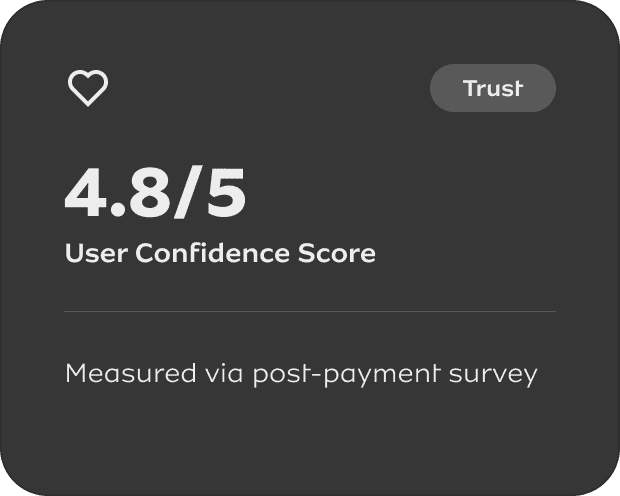

- Improved trust

01 — CONTEXT

The Business Reality

MTN operates as a digital financial ecosystem, not just a telecom product. The payment widget is embedded across merchant sites, processing millions of transactions monthly. It's a revenue-critical touchpoint where experience directly impacts conversion.

Business Problem

Payment failures were bleeding revenue and eroding merchant trust.

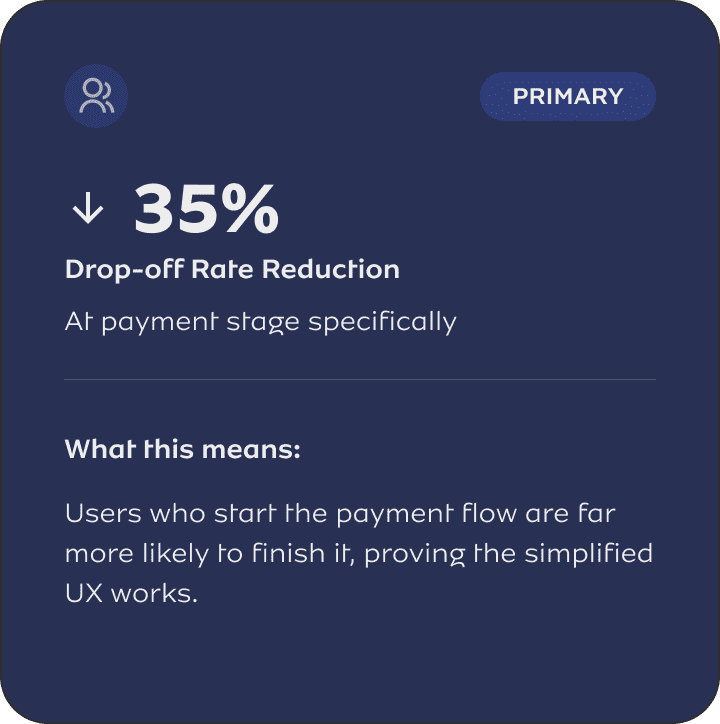

- 35% drop-off at payment stage

- Failed transactions impacting revenue

- Rising support costs

Users abandoned mid-flow, costing millions in lost GMV

Unclear error states led to repeated failures

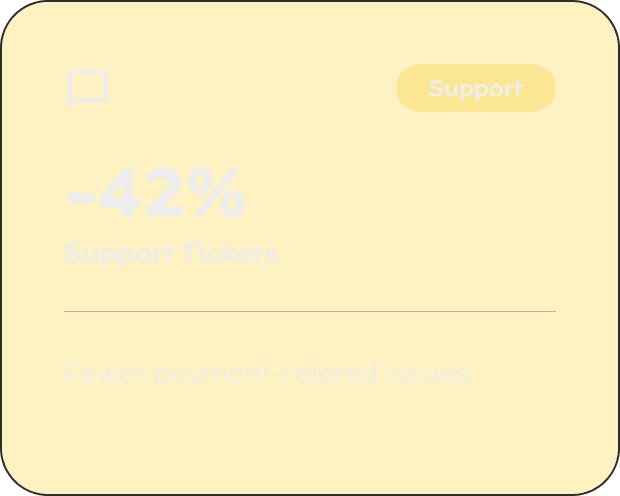

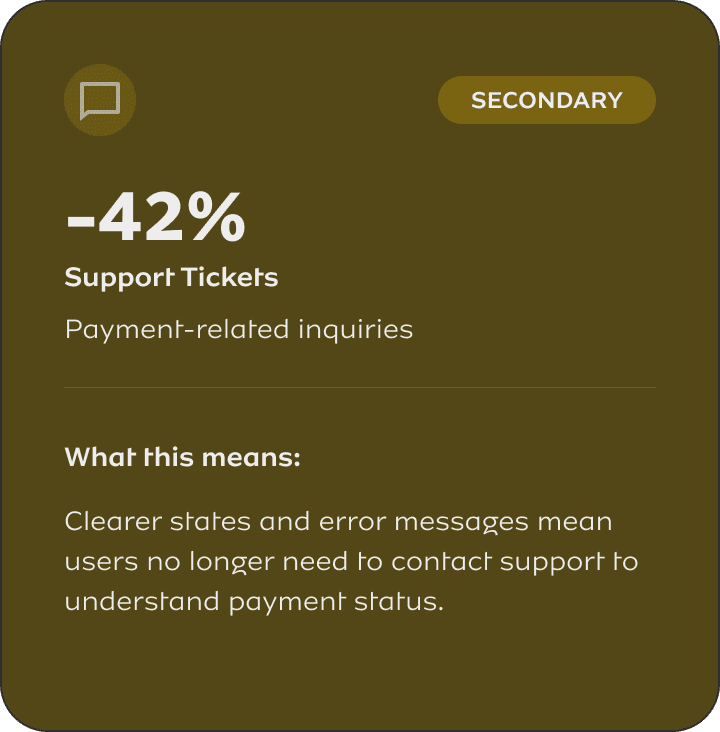

Payment-related tickets up 60% quarter-over-quarter

User Problem

People weren't failing payments, they were abandoning uncertainty.

- Zero visibility into payment status

- Cognitive overload during checkout

- Low trust in the system

"Did it work? Should I try again?"

Too many steps, unclear progression

No security signals, no error recovery guidance

In fintech, trust + clarity are not "nice to haves", they're revenue drivers. Every unclear state, every extra step, every missing feedback signal directly translates to abandoned payments and lost business.

02 - MY ROLE & OWNERSHIP

End-to-End Design

I owned the payment experience end-to-end, including:

- Product discovery

- UX strategy

- Interaction design

- UI execution

- Design system contribution

- Developer handoff + QA

I worked directly with:

- Product Managers (prioritisation, trade-offs)

- Engineers (technical feasibility)

- Business stakeholders (revenue + success metrics)

I had final say on UX direction, not just execution. This included trade-off decisions between business goals and user needs, feature prioritisation, and design system patterns.

03 - STRATEGIC APPROACH

Discovery → Strategy → Execution

Discovery & Research

Quantitative Analysis

- Analysed 2.3M payment transactions over 3 months

- Identified drop-off concentrated at steps 3 & 5

- Failed payments: 18% had unclear error messages

- Average completion time: 2m 47s (industry avg: 1m 30s)

Qualitative Insights

- 12 user interviews with recent payment failures

- Common theme: "I didn't know if it worked or failed"

- Trust concern: "Where's my money if it failed?"

- Support ticket analysis: 78% asked about payment status

Key Insights That Shaped Design

1. Users don't fail payments, they abandon uncertainty

When users can't tell if a payment is processing, pending, or failed, they close the window and try elsewhere. The problem wasn't technical failure — it was feedback failure.

2. Every extra step = perceived risk

In fintech UX, users equate complexity with unreliability. A 6-step flow signals "something could go wrong" while a 4-step flow signals "this is streamlined and safe."

3. Speed = perceived reliability

Faster doesn't just mean better UX in payments, it signals that the system works. A 45-second flow outperforms a 2-minute flow even if both succeed.

Design Strategy: 3 Core Pillars

Reduce Cognitive Load

Simplify the flow, remove unnecessary decisions, group related actions

Increase Trust Signals

Explicit payment states, security indicators, clear feedback at every step

Optimize for Speed

Faster flows, fewer interruptions, predictive defaults

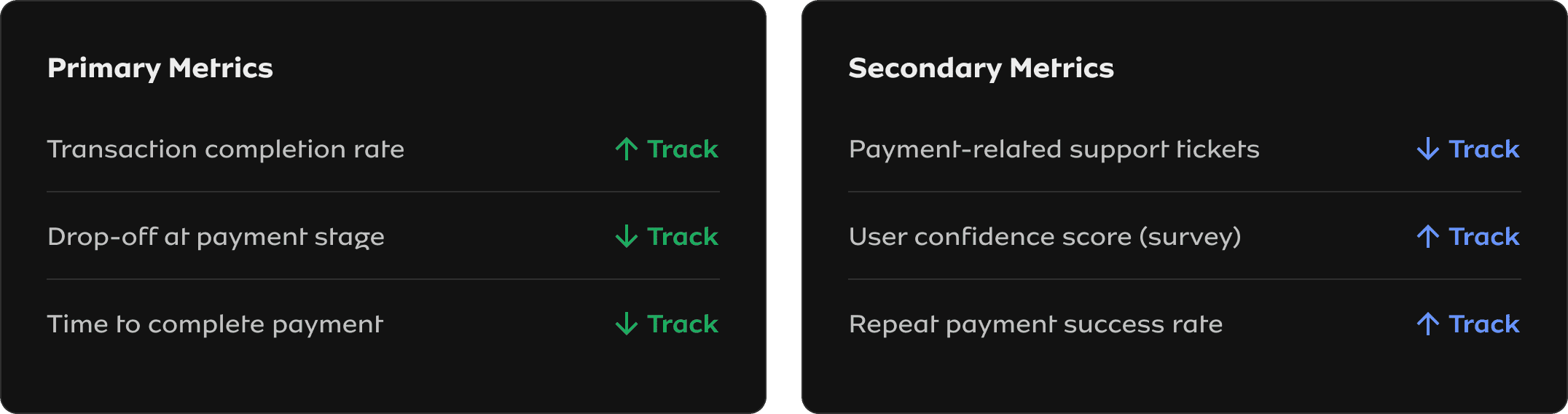

Defining Success (Before Building Anything)

04 - KEY DESIGN DECISIONS

Trade-Offs & Decision-Making

Every design decision involved trade-offs. Here's how I navigated them and what I chose to prioritize.

-

BEFORE

1. Login/Authentication (multi-step)

2. Select Payment Method (scattered options)

3. Enter Payment Details

4. Verify Information (separate screen)

5. Security Confirmation (OTP)

6. Complete Payment

AFTER

1. View Transaction Summary (amount + merchant)

2. Choose Payment Option (single dropdown)

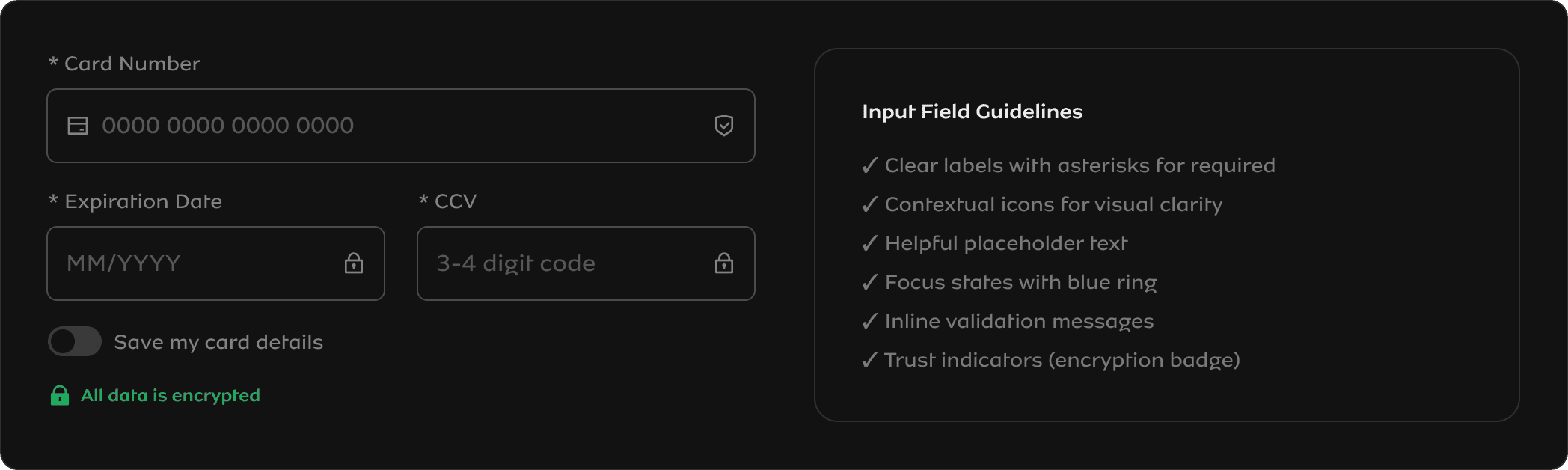

3. Enter Card Details (grouped fields)

4. Confirm Payment (one-tap)

⚠ TRADE-OFF: What We Lost

- Less flexibility in payment method selection

- Removed upfront verification step

- Combined authentication with first action

✓ TRADE-OFF: What We Gained

- 45% faster completion time

- Lower perceived complexity

- Reduced abandonment at each step

Why this trade-off was worth it: Data showed 80% of users used the same payment method. Optimizing for the majority case while keeping other options accessible (but not prominent) maximized conversion without significantly hurting flexibility.

-

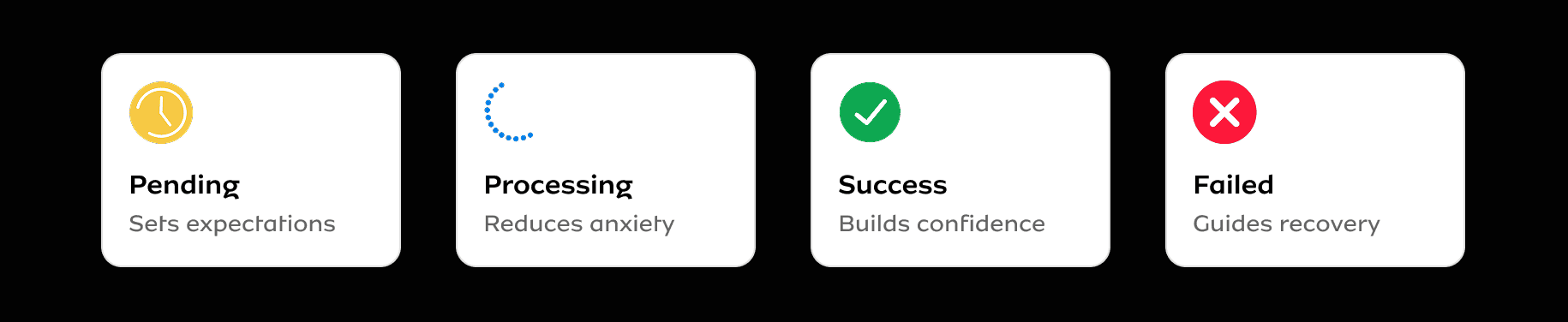

THE STATES

⏳

Pending

⚙️

Processing

✓

Success

✕

Failed

⚠ TRADE-OFF: What We Lost

- Increased UI complexity (4 states vs 1 generic)

- More design & engineering effort

- Additional edge cases to handle

✓ TRADE-OFF: What We Gained

- 78% reduction in "payment status" support tickets

- Users know exactly what's happening

- Clear next actions in failure cases

Why this trade-off was worth it: The old system showed a generic spinner for everything. Users couldn't distinguish between "initializing" and "bank is processing" and "waiting for confirmation." This caused anxiety and premature abandonment. The investment in explicit states paid off immediately in reduced support load and increased trust.

-

DESIGN PRINCIPLES

Primary action always in view

Button remains fixed at bottom, always accessible

Single visual hierarchy

Only one primary action per screen - no competing CTAs

Progressive disclosure

Advanced options hidden by default, accessible if needed

⚠ TRADE-OFF: What We Lost

- Less feature visibility (e.g., save card, payment history)

- Fewer upsell opportunities in the flow

- Some users may miss optional features

✓ TRADE-OFF: What We Gained

- 28% increase in CTA click-through

- Lower cognitive load = faster decisions

- Reduced decision paralysis

Why this trade-off was worth it: In payments, completion trumps discovery. We measured feature adoption and found that surfacing all options upfront actually reduced usage of those features — users were overwhelmed and skipped them. By hiding optional features behind progressive disclosure, we increased both payment completion AND feature adoption.

05 - THE SOLUTION

Final Design & Experience

A reimagined payment widget built on three pillars: simplified flow, explicit states, and action-focused UI. Below is the visual evidence of how each decision came to life.

The following sections show the actual UI I designed, with annotations explaining the reasoning behind each element.

→ Payment Flow comparison

→ All 4 payment states

→ Design system components

EVIDENCE 1 — SIMPLIFIED FLOW

Payment Flow: Before vs After

Visual evidence of how I reduced steps from 6 to 4, creating a linear, guided experience

-

Login/Authentication

Multiple verification stepsSelect Payment Method

Too many options, unclear hierarchyEnter Payment Details

Scattered form fieldsVerify Information

Separate review screenSecurity Confirmation

OTP or additional verificationComplete Payment

Uncertain outcome

❌ High drop-off rate

Users abandon due to cognitive overload

-

View Transaction Summary

Clear amount & merchant infoChoose Payment Option

Single dropdown, clear hierarchyEnter Card Details (Once)

Grouped fields, encrypted messageConfirm Payment

One-tap action with clear CTA

✓ +20% transaction completion

Fewer steps = less friction = higher conversion

✓ Trust signals visible throughout

EVIDENCE 2 — PAYMENT STATES

All Four Payment States

Why Explicit States Matter

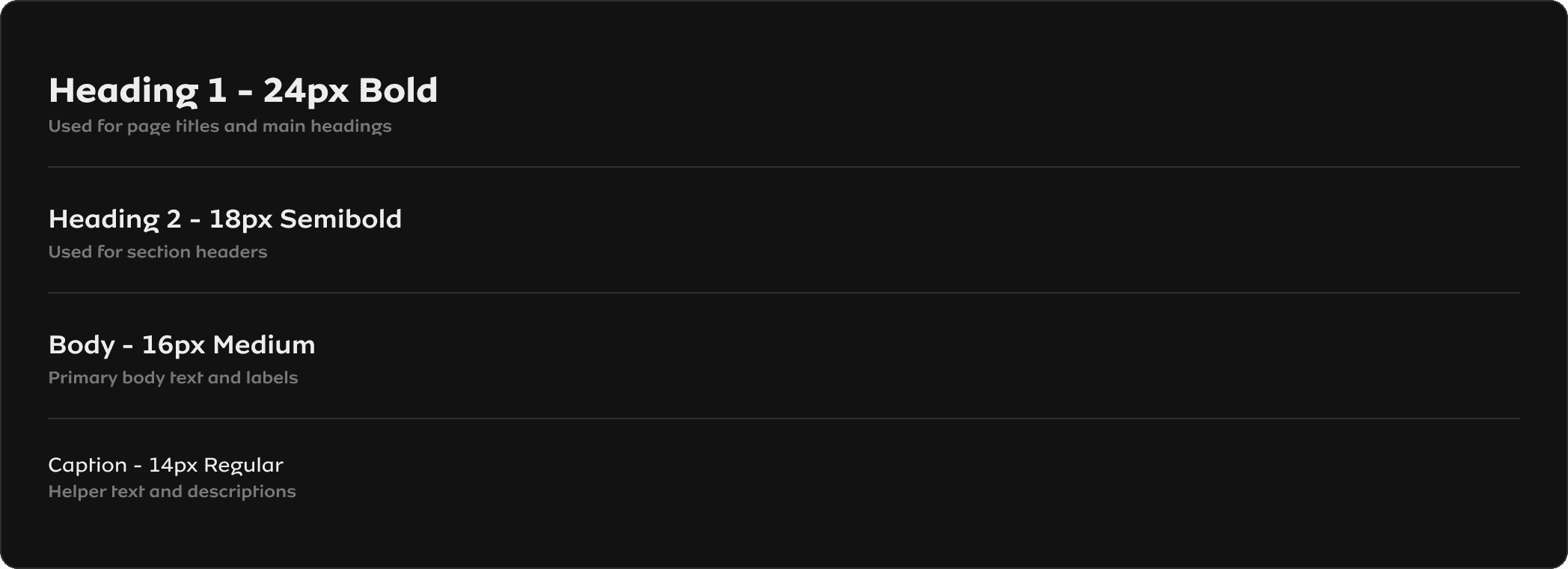

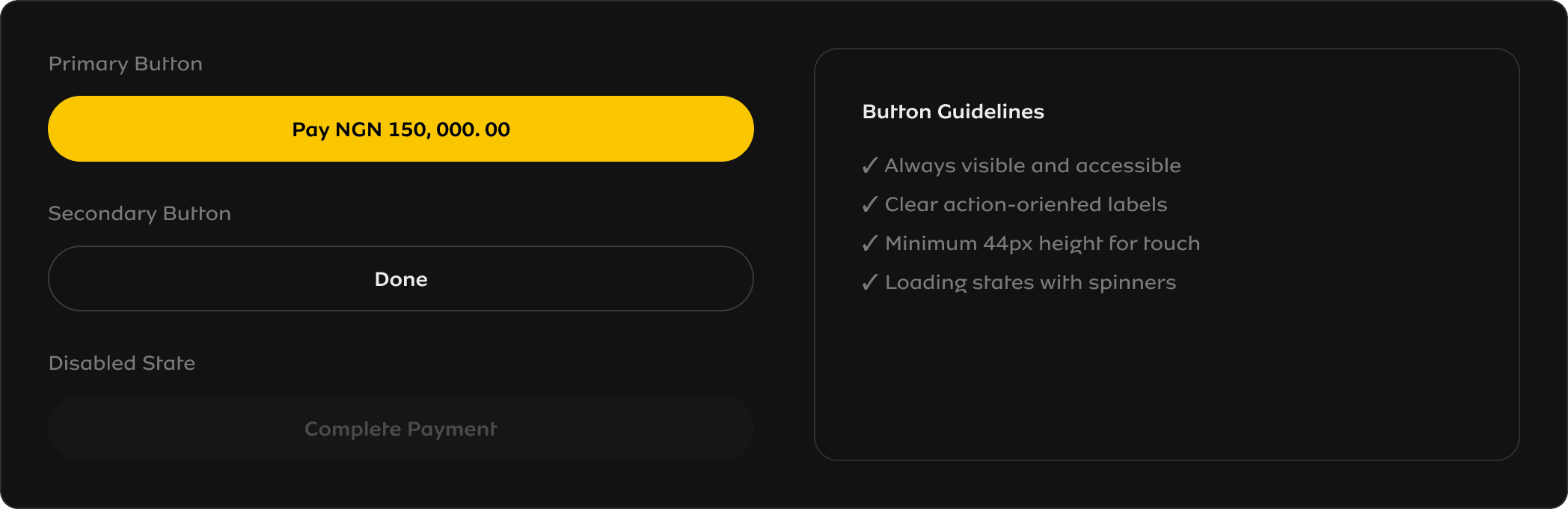

EVIDENCE 3 — DESIGN SYSTEM

UI System & Components

Scalable design system ensuring consistency across the payment experience

Color System

Typography Scale

Button Components

Form Input Components

EVIDENCE 4 — IMPACT METRICS

Measured Impact Visualization

Quantified results showing the business value of design decisions

06 — OUTCOMES & IMPACT

Measured Business Results

The redesign launched in a phased rollout over 6 weeks. Here's what happened.

07 — REFLECTION

Key Takeaways

What Worked Well

✓ Data-driven decision makingAnalyzing 2.3M transactions gave us confidence to make bold simplifications. The metrics validated our assumptions.

✓ Phased rollout strategy

Catching the mobile keyboard bug at 10% traffic saved us from a major incident. Always de-risk payments.

✓ Clear success metrics upfront

Defining what "good" looks like before designing prevented scope creep and kept us focused on outcomes.

What I'd Do Differently

→ Earlier engineering involvementWe discovered technical constraints around payment state webhooks late. Should have prototyped with eng in week 1.

→ More merchant stakeholder input

We focused heavily on end-users but could have gathered more feedback from merchants who embed the widget.

→ Accessibility audit earlier

We caught and fixed keyboard navigation issues in QA. Should have been part of the design phase, not validation.

Core Insight

Designing payments isn't about making beautiful UI; it's about reducing uncertainty, building trust, and enabling fast decisions under pressure.

Every pixel, every word, every transition exists to answer one question: "Is my money safe, and did this work?" When you optimize for that, conversion follows naturally.

Simplified Payment Flow

Reduced from 6 fragmented steps to 4 linear, focused actions